We’re about to have more real estate “bubble” conversations. Why? Because prices are very close to where they were at the previous peak of the market. Here’s a few things that come to mind when these conversations come up. Then for those interested I have a big monthly market update. Anything to add?

Higher prices fuel conversation: As prices rise, it inflames conversation about a real estate “bubble”. Media outlets cover this topic of course, but it’s also on the mind of the public.

Stats are VERY close to the peak: Markets throughout the country are different, but in Sacramento most price metrics are getting very close to the peak from 2005. In fact, the average sales price in the Sacramento region is now the SAME as it was back then.

No formula: As a friendly reminder, there is no “bubble” formula that says the market will plummet if we get back to prices from 10+ years ago.

Hello inventory: As news of high prices gets out there, some sellers will put their homes on the market thinking we are at the top. So let’s watch inventory very closely in coming time.

Normal seasonal slowing: Right now the market is slowing, and some are saying, “It’s starting to turn. Pop. The Bubble is happening!!!” Here’s the thing though. Markets tend to have a seasonal cycle where things are hot and then they cool off. When the market begins to soften each year we tend to hear a little more doom & gloom because sometimes we confuse a seasonal slowing with the market tanking. At the moment the stats in Sacramento look normal for the season and don’t indicate the market has made a big turn down, so I’ll keep saying that unless I have a reason not to. Make sense?

Normal seasonal slowing: Right now the market is slowing, and some are saying, “It’s starting to turn. Pop. The Bubble is happening!!!” Here’s the thing though. Markets tend to have a seasonal cycle where things are hot and then they cool off. When the market begins to soften each year we tend to hear a little more doom & gloom because sometimes we confuse a seasonal slowing with the market tanking. At the moment the stats in Sacramento look normal for the season and don’t indicate the market has made a big turn down, so I’ll keep saying that unless I have a reason not to. Make sense?

Less room: There is less room for prices to increase unless the job market and wage growth really start to move. So it seems logical for the market to slow down. Yet there are many dynamics that make prices move, and nobody has a crystal ball to say exactly what prices will do in the future.

Don’t forget Inflation: This might sound anal, but let’s get technical about comparing older prices with today’s prices. We’ve had thirteen years of inflation since 2005, and that means it’s gotten more expensive to buy the same goods today than it was in the past. For instance, the peak of the market in Sacramento saw a median price at $395,000 in 2005, but when adjusting that figure for inflation with an inflation calculator, a price at $395,000 in 2005 would technically have the same purchasing power of $511,000 today. So as today’s median price approaches $395,000, we have to realize it’s really not the same $395,000 as it was in 2005 because of how the value of the dollar has changed over time.

But the market doesn’t care about inflation: Okay, let me now throw a curveball. It’s important to understand how inflation works for the sake of comparing older stats, but I don’t think most buyers and sellers actually care about inflation. They don’t say, “Sweet, prices today look like they’re the same as 2005, but technically they’re lower because of inflation.” No, people tend to see prices and say, “Holy heck, we’re back to the peak.” I’m not dismissing the need to understand how inflation works, but only being real about how the bulk of buyers and sellers tend to think. Besides, it doesn’t matter how close we are to the previous peak anyway because there is no formula that says the market will “pop” at that level.

Preaching doom: Some preach doom & gloom, and that’s fine. My advice though? Be realistic about your ability to predict the future. Some have been making annual real estate predictions about how the market is about to collapse, and I’m hearing many say the big change is now coming later this year or in 2019. The problem is when these predictions don’t come true the “prophecies” simply get pushed back another year. The irony is if a person keeps making the same prediction every year, at some point that person could be right.

Seeing only red flags: It’s getting less affordable. The economy isn’t that great. Interest rates are rising. Home prices have outpaced wage growth. Lenders are getting more creative with financing. These are red flags for sure. But let’s remember just because unhealthy elements exist in a market does not mean it’s starting to crash. My advice? Be honest about the red flags, but let actual stats inform what you say and think about the market. Keep in mind many articles in coming time are going to preach doom, but take a step back from the articles and look to the stats. What do the stats say? And what is the mood among buyers and sellers in the market? That’s the only thing that matters.

Open letter to worried buyers: Last year I wrote an open letter to buyers worried about another housing bubble. I have some practical advice and tips in there in case it’s relevant.

I hope that was interesting or helpful. Anything to add?

-—-—- Big monthly market update (long on purpose) ———–

We saw what we would expect to see last month. It felt like a normal May. Well, actually it was the strongest May of sales volume since 2013. Prices ticked up again, it took three less days to sell, and inventory remained sparse. Overall the stats are glowing, but it’s important to recognize the market is starting to slow for the season. We are seeing way more listings hitting the market, and this is transferring some power from sellers to buyers. We are also seeing more price reductions. In a few months we will likely see this slowness in the stats, but for now check out some glowing numbers below.

We saw what we would expect to see last month. It felt like a normal May. Well, actually it was the strongest May of sales volume since 2013. Prices ticked up again, it took three less days to sell, and inventory remained sparse. Overall the stats are glowing, but it’s important to recognize the market is starting to slow for the season. We are seeing way more listings hitting the market, and this is transferring some power from sellers to buyers. We are also seeing more price reductions. In a few months we will likely see this slowness in the stats, but for now check out some glowing numbers below.

The previous “bubble” vs now:

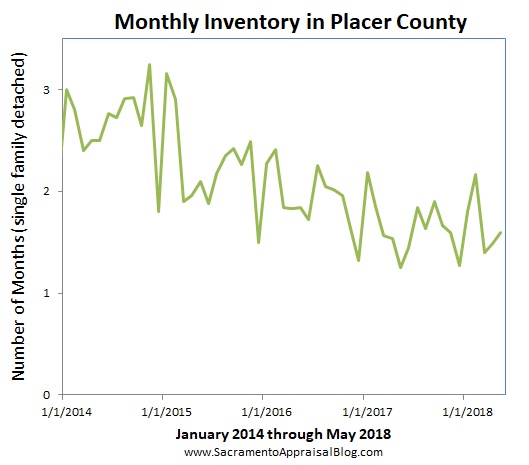

1) Housing inventory: Since late last year housing inventory has begun to increase subtly. Right now we have 1.5 months of housing supply whereas one year ago we had 1.26 months of supply. Some might interpret this to mean the market has begun to collapse and really change directions, but this is still a very anemic level of housing supply, and the market has been able to handle this change easily because of strong demand. For reference, when the market collapsed in 2005 inventory literally doubled in 90 days from the summer to the fall. That’s a far different story than what we’ve seen so far this year with a minor uptick in inventory over the past two quarters.

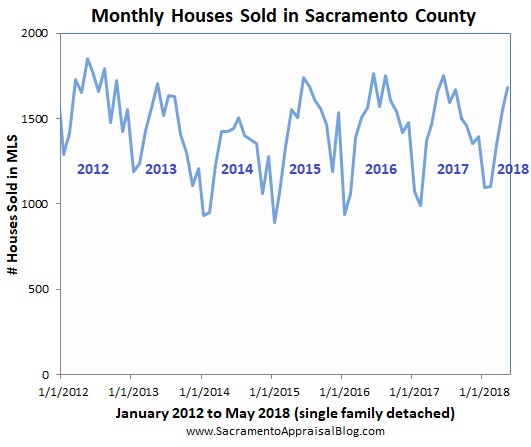

2) Sales volume: If we did have a “bubble” and it burst, I would expect to see more listings hit the market and most likely a drop in sales volume. In 2005 the market changed and properties simply stopped selling as you can see below. In one year sales volume literally dropped by 43%. Yikes!! In contrast, right now sales volume has been very steady. Let’s keep an eye on sales volume and inventory though because both metrics might help us gauge if the market really is changing. Remember though, before we see a change in sales, we’ll hear of a change in the mood of buyers and sellers. Thus the trend always happens in the listings first before we start to see it in the sales. That’s why the word on the street is so important in real estate (agents, please keep emailing me to let me know what you are seeing out there).

I could write more, but let’s get visual instead.

DOWNLOAD 61 graphs HERE: Please download all graphs here as a zip file. See my sharing policy for 5 ways to share (please don’t copy verbatim).

SACRAMENTO COUNTY (more graphs here):

SACRAMENTO REGION (more graphs here):

PLACER COUNTY (more graphs here):

DOWNLOAD 61 graphs HERE: Please download all graphs here as a zip file. See my sharing policy for 5 ways to share (please don’t copy verbatim).

Questions: What are you hearing buyers and sellers saying about the market? Do you think the market has turned or are we seeing a seasonal slowness? I’d love to hear your take.

If you liked this post, subscribe by email (or RSS). Thanks for being here.

Ryan…..

Great article! I have been getting into more of these conversations with both buyers & sellers. Another factor that I am seeing is immigration from Bay area and So. Cal. This creates demand and keeps inventory low. I have also noticed that “Bay area” buyers think we are still a great buy (based on Bay values),and are ready to make offers immediately. I wonder if there is a way to track population growth in Sac Area vs inventory.

Another factor that created the big bust in 2005 were lenders that gave money to unqualified buyers. Today’s lenders are still making buyers jump through hoops and have”skin” in the game even if it is only 3%. Buyers will be less likely to walk away from their homes if/when the mark slows.

Thanks for your excellent blogs!

Thank you John. I appreciate your kind words and your comments are excellent.

One of the struggles here from a stats perspective is it’s hard to say exactly how many Bay Area buyers are influencing the numbers. I don’t buy into the notion that Bay Area buyers are gutting the market by any stretch. It’s just not true based on conversations with agents and thinking logically about some of the metrics. Some say, “Bay Area buyers are paying cash for everything.” Well, only 15% of all sales are cash right now, and that’s actually pretty normal (it was 30% at the investor peak in 2013). Yet because of a presumed influx of Bay Area buyers in recent years, it is possible to mask the market a bit. What I mean is if local buyers cannot afford the market, it’s possible for those buyers to be squeezed out and for us to not see much price impact in the stats because Bay Area buyers can pick up their slack. This is just something we have to keep in mind in the background. Unfortunately I am not aware of a way to parse who exactly is buying beyond what type of loans are happening in the market. I’d have to rely on a big data firm for that sort of information. I know the Greater Sacramento Economic Council has discussed there are 23,000 Bay Area residents moving to the market each year. For reference, wee only have about 28,000 single family detached sales in the region each year (not all the residents moving here are actually buying).

You are so right about the hoops. It is not easy to get a loan, even if the loan is more risky. I bought a house in 2015 and as a self-employed person I thought the lender just didn’t want to do the loan. I almost felt like giving up because of the incessant requests for profit / loss statements, financial details, etc…

Wow, in Portland, we were back to peak prices in 2015. Where has Sacramento been?

Portland is such a trend-setter… In truth our median price declined a whopping 59.5%, so it is no little thing to “recover” back to that price point. I’m thinking many markets did not decline by that much. When the market collapsed in 2005 we really struggled in Sacramento. I’d guess our economy has not been as vibrant either compared to Portland. I need to make it up there again soon Gary…

Ryan, you are a wizard and a genius! Great work. It’s interesting – the Fresno/Clovis area experienced a lot of Bay Area or LA cash buyers during the boom as well, fueling Fresno/Clovis values way higher than they ever should have been. My guess is that it declined relatively similar to the Sac area – somewhere around that 60% point. In Clovis, the home I sold a couple years ago is still not recovered to its peak – it’s still about $50K less than its peak. Meanwhile, here in Utah we are well past the peak, so it’s fun to have that conversation since most people don’t experience multiple markets.

Thanks Jacob. I’m not sure I’m either of those, but I’ll take it as a big compliment. 🙂

I appreciate hearing your take on multiple markets. It just goes to show when someone talks about the “national housing market,” there really isn’t a one size fits all description of what the market has done. I would imagine Fresno was hit really hard too. I find in Sacramento some classic neighborhoods reached their previous peak already last year or the year before, but that hasn’t been the case with county-wide stats. The condo market in many areas is nowhere close to the previous peak either and vacant land sales are also much more subdued than they used to be. I find 2-4 unit sales are also a bit more subdued, but that’s not the case for 2-4 units in Midtown / Downtown. All things said, I’m reminded that even if a market as a whole is trending at a similar price point to the past, it doesn’t mean every neighborhood, price range, or property type is experiencing that same trend.

When the “bubble” burst we saw neighborhoods with higher values tended to decline less compared to neighborhoods with lower values (and more adjusted rate mortgages). Since higher-priced neighborhoods had less of a decline, it basically enabled them to reach their peak more quickly. In contrast, lower-priced areas have had to climb very far up after avalanche-type declines.

Anyway, I don’t mean to ramble, but that’s what your comment evoked.

Have been working in Hawaii on the island of Maui for about twenty years. The data is interesting with predominately second home buyers as price levels exceed most local economic conditions. It is also highly seasonal. Trends can easily be skewed as data limited and prices are wide. Many small sub markets to research. I like your articles and how you track trends. Helps me with my work. Thank you Ryan.

Dan

Hi Dan. Thank you so much for the comment. And by the way, now that you have a comment approved, you’ll never be moderated. Anyway, I appreciate the kind words. I’m a little jealous of where you work too…. Though it sounds challenging to be able to really see the market or trend in the midst of such a data shortage. I wonder when pulling comps if you use sales from other islands too or stick to Maui only. Thanks again.

Hi John,

Good stats and graphs but you’ve left out the component of rate hikes. That inverse relationship to home values is starting to impact sales and I’ve noticed prices starting to drop and homes coming back on the market after falling out of escrow. I’m a realist and as Tom Sullivan stated after the great recession the exponential growth was unsustainable due to the rapid increase in home values. Real estate doesn’t ordinarily gain double digit appreciation annually. From 2000-2005 the growth was approximately 40%…that’s 8% per year. We’ve been seeing the same growth since 2013. I’ve been selling since 1999 and when I asked the old timers how we dodged the bullet in 2003 no one had an answer. We now know how the banks manipulated the system. Again I’m wondering how are we able to dodge the bullet…time will tell. I don’t want to be a naysayer but somethings about to give…I’m just not that smart to figure it out.

Thanks Beth. I appreciate your thoughts. Please pitch in any time, even if you disagree.

I did mention rising rates as a “red flag” above. I think you’re right that we need to watch rates, and it can bring change in the market to a certain extent – especially at the lower end where buyers are struggling with affordability already. Unfortunately some buyers will be priced out of the market because of rising rates. But are there enough other buyers waiting in line to buy in their place? Right now I’m guessing there are. At some point if prices get too high, the market will theoretically resist those prices though. Lenders can of course create products to help compensate for rate increases. That doesn’t sound very healthy to me, but I wouldn’t be surprised either.

Rate increases are a big deal, but they are not the only show in town either. The interesting thing to consider is that mortgage rates have basically declined since the early 80s, yet we’ve had a couple real estate cycles in between where values declined despite an environment of rates generally declining. Even during the last “bubble” I’d say rates changing was not the factor that caused the “pop”. I don’t say this to downplay the power of rates. I’m only reminded there are many other factors that make value move beyond rates.

I share your concern about prices increasing. It’s really not sustainable forever without wage growth, economic growth, etc… In each appraisal when I talk about what the market is doing I have a closing line where I say, “Values increased substantially in the Sacramento area since 2012, and such quick appreciation may not be sustainable over the long haul. It is not known what values will do in the future.”

Let’s keep watching the softening you mention. Is it seasonal or is it something more? Time will tell. And that’s exactly why we need to watch closely.

Thanks again Beth. I always appreciate your take.

Great points, Ryan. I think you pointed out something important and that is buyer mood. I guess this is the same as consumer confidence? If buyers are confident about the future then that may keep the economy rolling. Another point is that while some areas may be reaching peak still others may not be, so we have to look at the local numbers and try to avoid making a blanket statement about the country as a whole.

Thank you Tom. Yes, that’s what I mean. How are buyers feeling about the market? Are they confident? Are they pulling the trigger? Or they standing off? The word on the street matters greatly.

I agree on different markets. Well said. The reality is even in a local market we might have different segments of the market that are reaching “peak” prices, but some are not. Thus condos, commercial properties, and vacant land might be trending totally different than single family detached homes. Moreover, we might have some neighborhoods doing better than others. Your point is so key because there are thousands upon thousands of sub-markets throughout the country, so we can’t really easily sum all of them up with some neat article about the health of the “national” real estate market. On a similar note, this is why I don’t pay too much attention to statewide real estate data. Yes, it’s worth looking at maybe, but what’s happening on a larger scale really might not translate to every single market. Local > state / national.