How are appraisers handling concessions to the buyer? Could a seller credit damage the chance of appraising at the purchase contract? These questions weren’t asked a year ago, but welcome to the 2023 housing market.

UPCOMING (PUBLIC) SPEAKING GIGS:

1/18/23 WCR Market Update in Cameron Park (register here)

1/19/23 Big market update at SAR on Zoom (register here)

1/20/23 NARPM Luncheon

1/23/23 Residential RoundUP on Zoom (register here (free))

1/26/23 How to Crush Lead Gen (for real estate) (register here)

1/27/23 Q&A Appraiser Marketing (free for appraisers only) (sign up here)

2/8/23 SAFE Credit Union “Snacks & Facts” (for RE) (register here)

3/10/23 PCAR Market Update Lunch & Learn (detailed TBD)

3/28/23 Downtown Regional MLS meeting

4/1/23 NAA Conference in Sacramento

GOOD NEWS FOR BUYERS

Buyers are getting more from sellers lately. Last month 51.5% of all sales in Sacramento County had some form of a concession. Sellers are tending to give things like credits for closing costs, credits for repairs, rate buydowns, etc… Sellers, be ready to negotiate with buyers and offer more if needed. And buyers, get all the market will give you.

HOW DO APPRAISERS VIEW CONCESSIONS?

Question: When a buyer comes in over list price and asks for a concession from the seller, how is that viewed from an appraiser’s mindset?

Answer:

1) No effect on value: The appraiser needs to look to the comps to establish value. Bottom line. The seller can give 3% or more if the lender allows, but this shouldn’t have any bearing on the appraised value theoretically because the proof of value is found in the comps – not the terms of the contract. In other words, if the comps suggest a value at $500,000, it doesn’t matter if the subject is in contract at $500,000 with the seller giving 3% back for closing costs. However, if the only comps at $500,000 are ones with fat credits, and comps without any concessions are coming in closer to $485,000, then that tells us the comps with concessions are maybe closing high due to the concessions. This is where an appraiser might adjust the comps down in the appraisal report if it looks like the market isn’t willing to pay $500,000 without the extra sweetener to get the deal done. And this is where agents establishing a list price really want to pay close attention to what’s happening with concessions in the comps. Don’t just look at the final sales price.

2) Inflated contract price: All that said, when a property has been on the market for a long time, and it gets into contract at a higher level with a huge credit, it’s only human to wonder whether it’s really worth that amount. It sounds a bit suspect, right? In other words, would buyers really pay the contract price if the seller wasn’t giving a fat concession? This is a viable question, and the appraiser is going to record the full listing history of the subject property and scrutinize the terms of the contract in the appraisal report. This means the underwriter is going to see everything too. But still, the most weight needs to be given to the comps, so even if the contract price initially looks iffy based on the listing history alone, appraisers have to be careful to be objective about looking to the comps for value rather than the listing history alone. There is no ignoring the listing history though because it might be a clue about value. But then again, maybe there was a problem tenant who wouldn’t allow access, a lack of open houses, or some other reason why the property was on the market for longer than expected.

3) But the seller wants a higher price: A strategy I see sometimes today is to raise the price and give the buyer a credit back for the amount the price was raised. The idea is to help the seller net more and keep the buyer happy with a credit. Look, it’s fine if the market allows the seller to do this, but sometimes properties are countered beyond what is able to be supported by the appraiser. Remember, the appraiser is looking at all the details of the comps – not just the closed price. Sometimes I hear people say, “Bro, the property closed at $500,000, so it’s a good comp.” Okay, but if this unit also had a 3% credit for closing costs, the appraiser has to consider if that credit inflated the price too. My advice? Be aware of countering too high beyond what the comps suggest is reasonable, and remember the appraiser’s job is NOT to ratify the contract price.

THE MARKET IS HEATING UP FOR THE SPRING:

By the way, the market is beginning to heat up for the spring. I’ve been talking about expecting this. Even during a declining trend, we historically see more attention on the market in the spring season. I’m hearing of more showings, some competition, and phones are ringing. Granted, it’s still crickets for lots of listings, so it would be a big mistake to say today has early 2022 aggressive vibes. The tough part about January is buyers are hungry for fresh listings, but they are slow to come to the market. More on that soon.

Thanks for being here.

MARKET STATS: I’ll have lots of market stats out this week on my social channels, so watch Twitter, Instagram, LinkedIn, and Facebook.

Questions: What sort of concessions are you seeing offered right now? Anything else to add? I’d love to hear your take.

If you liked this post, subscribe by email (or RSS). Thanks for being here.

DOWNLOAD 70+ visuals

DOWNLOAD 70+ visuals

The market ripened early this year. Buyers have simply been ready before sellers. On one hand listings and sales have been at fairly normal levels for the first two months of the year, so we can say the market is normal in that regard. But buyer demand really took off last month as pendings in the regional market were up by almost 30% compared to last February. This is the part that is not normal, and why we can say the Spring market ripened early.

One Paragraph to Explain the Market: Well-priced listings are going quickly and experiencing multiple offers, but otherwise properties are sitting on the market if they are not priced correctly. Buyers have been anxious to get into contract, but at the same time they seem to be showing discretion by not readily pulling the trigger on homes with adverse locations or issues. This has led to a sense of many current listings feeling like leftovers since they’ve been well vetted like thrift store clothing. The good news is we are reaching the time of year where more listings should be hitting the market to help alleviate the pressure of a lack of good inventory. Lastly, it took a few less days to sell last month, inventory decreased, and the sales to original list price ratio increased (all normal in Spring).

NOTE: I am posting once a week now, and this means my big monthly post will have less text, but a few more graphs (Placer, Sacramento County, & Regional Market).

Two ways to read this post:

DOWNLOAD 45+ graphs HERE for free (zip file): Please download these 45+ graphs here as a zip file (or send me an email). Use them for study, for your newsletter, or even some on your blog. See my sharing policy for 5 ways to share.

SACRAMENTO COUNTY:

PLACER COUNTY:

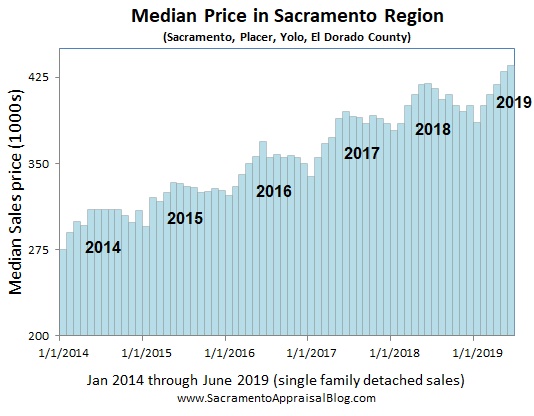

SACRAMENTO REGION (Sac, Placer, Yolo, El Dorado):

Questions: What is driving buyers to get into contract? Is it low rates? Is it a sense of needing to get in a home before values rise too quickly? What do you think?

If you liked this post, subscribe by email (or RSS). Thanks for being here.